Our research team evaluated 23 instant payout technologies used by businesses across the United States. We analyzed each option using the following weighted criteria:

- Settlement Speed (30%): How quickly funds become available to recipients

- Cost per Transaction (25%): Total fees, including transaction costs and network charges

- Transaction Limits (20%): Maximum amounts per transaction and daily caps

- Availability (15%): 24/7/365 access versus business-hours-only processing

- Use Case Fit (10%): Industry-specific advantages and specialized capabilities

After applying this algorithm, we rank-ordered all options and selected the top performers. The table below breaks down how the best instant payout options compare across the key factors that matter most to businesses evaluating instant payment technologies, with in-depth reviews to follow.

Best Instant Payout Options

Businesses looking for two-way payment options should consider that these all make great instant payment options for incoming funds as well. However, the following subsections dive deeper into each to make decision-making a bit more clear-cut.

1. Same-Day ACH: Best for Gig Platforms & High-Volume Payroll

Same-Day ACH transforms traditional ACH processing by enabling funds to settle on the same business day rather than the standard 1-3 day window. The system processes transactions in two daily windows, allowing businesses to initiate payments until mid-afternoon and still achieve same-day settlement.

With a transaction limit of $1 million, costs ranging from $0.05 to $0.30 per transaction, and coverage of every bank in the US, Same-Day ACH delivers the optimal balance between speed, availability, and affordability for high-volume payment scenarios. This is why they are our #1 pick for the best instant payout options of 2026.

The platform particularly excels for gig economy platforms that need to disburse earnings to thousands of workers simultaneously without the premium costs of true real-time rails. Real-time payments are also not available at every bank, which can make it difficult for businesses looking to disperse or accept payments to/from a disparate group of people working with a number of different banks. Same-Day ACH provides a cost-effective middle ground and wider reach when true instant settlement isn't critical or available. These features also make it one of the best instant payment options for incoming funds.

- Settlement Speed: 4-6 hours during business hours, with two daily processing windows

- Cost per Transaction: $0.05-0.30, significantly lower than wire transfers or instant options

- Transaction Limit: $1 million per transaction as of 2025

- Best For: Gig platforms, payroll processing, high-volume merchant disbursements

2. RTP (Real-Time Payments): Best for B2B High-Value Transactions

RTP from The Clearing House represents America's first true real-time payment network, launching in 2017 with immediate settlement capabilities that transform B2B cash flow dynamics. Unlike Same-Day ACH or wire transfers, RTP settles transactions in seconds with complete finality; no reversals, no delays, no waiting for clearing windows. The network recently increased its transaction limit to $10 million, positioning it as the premier instant payout option for corporate treasury operations.

RTP costs between $0.01 and $0.05 per transaction, delivering 80% cost reductions compared to wire transfers while providing faster settlement. Its main drawback as of now is availability, though this is improving with each passing year. As of December 2025, RTP reaches 65% of U.S. checking accounts, with 481 participating financial institutions.

- Settlement Speed: Seconds with immediate finality and no reversals

- Cost per Transaction: $0.01-0.05, dramatically cheaper than wires for high-value transfers

- Transaction Limit: $10 million per transaction as of February 2025

- Best For: B2B high-value transactions, corporate treasury, time-sensitive settlements

3. Wire Transfers: Best for Large B2B & International Payments

Wire transfers remain the gold standard for large-value transactions and international settlements despite their higher costs and slower processing compared to modern instant payment rails. Domestic wire transfers typically settle on the same business day with costs ranging from $15-50, while international wires take 1-3 business days and can cost $35-80 or more, depending on intermediary banks. The key advantage of wire transfers is their unlimited transaction size and universal acceptance across all financial institutions globally.

For businesses requiring international settlements or transfers exceeding the $10 million RTP limit, wire transfers provide the established infrastructure that newer payment rails cannot yet match. However, banks charge $15-50+ per wire transfer, making them 300-1,000 times more expensive than Same-Day ACH for equivalent domestic transactions.

- Settlement Speed: Same business day (domestic), 1-3 days (international)

- Cost per Transaction: $15-50 (domestic), $35-80+ (international) plus intermediary fees

- Transaction Limit: No limit, supporting transactions of any size

- Best For: Large B2B payments exceeding $10M, international settlements, real estate closings

4. Digital Wallets: Best for Consumer Payouts & Small Business

Digital wallets like PayPal, Venmo, and Zelle democratize instant payouts for consumers and small businesses without requiring sophisticated payment infrastructure. Zelle offers free instant transfers between bank accounts, while PayPal and Venmo charge 1.75% for instant transfers but offer free options with 1-3 day settlement. Transaction limits vary significantly by platform; Zelle supports up to $100,000 through participating banks, while Venmo caps transactions at $5,000.

Over 435 million active PayPal accounts worldwide create instant credibility for businesses, potentially increasing conversion rates by 15-20%. However, these platforms typically prohibit use for certain business categories and may impose sudden account holds, making them unreliable for high-risk or high-volume operations.

- Settlement Speed: Instant (with fees) or 1-3 days (free standard)

- Cost per Transaction: Free (standard timing), 1.75% (instant withdrawal)

- Transaction Limit: $5,000-$100,000, depending on platform and account verification

- Best For: Consumer payouts, P2P transactions, small business payments under $5,000

5. FedNow: Best for Insurance Claims & Emergency Disbursements

FedNow launched in July 2023 as the Federal Reserve's answer to RTP, providing government-backed instant payment infrastructure available to all U.S. financial institutions. The network has experienced explosive growth, processing $245 billion in Q2 2025 compared to just $492 million in Q2 2024, which is a staggering 49,000% year-over-year increase. In June 2025, the Federal Reserve increased FedNow's transaction limit from $500,000 to $1 million, expanding its utility for mid-sized business transactions.

The platform particularly excels for insurance claims and emergency payouts where speed directly impacts customer well-being. FedNow's 24/7/365 availability means insurers can process claims immediately rather than waiting for traditional banking windows, transforming customer experience during emergencies.

- Settlement Speed: Seconds with immediate availability for recipients

- Cost per Transaction: $0.01-0.045, competitive with RTP for instant settlement

- Transaction Limit: $1 million as of June 2025 (up from $500K)

- Best For: Insurance claims, emergency disbursements, gaming/gambling industry

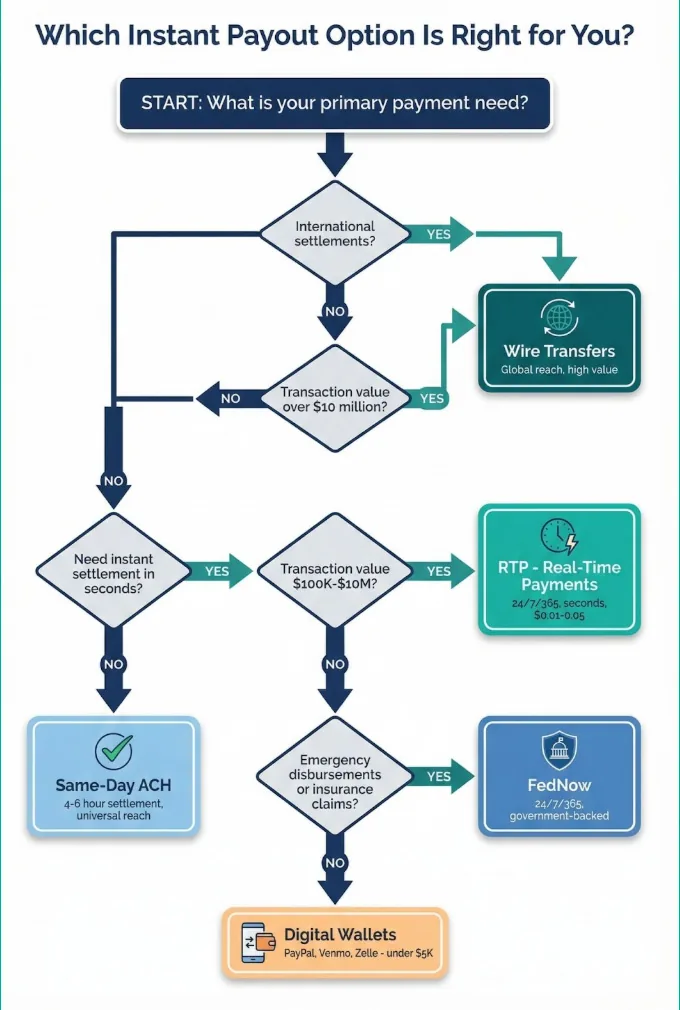

Choose Same-Day ACH if: You process high volumes of moderate-value payments ($1,000-$100,000) where same-day settlement meets customer expectations and cost efficiency matters more than instant availability.

Choose RTP if: You need true instant settlement for high-value B2B transactions ($100,000-$10 million) or if you operate across time zones that require 24/7 availability.

Choose Wire Transfers if: You're sending transactions exceeding $10 million, require international settlements, or you need universal acceptance regardless of the recipient's banking infrastructure.

Choose Digital Wallets if: You're disbursing to consumers or small businesses who prefer familiar platforms, and the transactions are under $5,000 in low-risk industries.

Choose FedNow if: You need instant emergency disbursements, process insurance claims requiring immediate customer relief, or operate in gaming where 24/7 instant deposits drive satisfaction.

For businesses requiring a comprehensive payment infrastructure that supports multiple instant payout options, working with a specialized payment processor provides flexibility to optimize for each transaction type. SeamlessChex offers Same-Day ACH, RTP capabilities, and traditional payment methods through a single integration, allowing businesses to route each payout through the most cost-effective rail while maintaining instant payout options when speed matters most. We also offer the same level of variety for instant payment options for incoming funds, with the addition of credit card processing.

Ready to optimize your instant payout infrastructure? Apply now to explore how SeamlessChex supports the best instant payout options for your specific business needs.