As a business owner, Seamless ACH has helped to significantly reduce the number of checks we have to put in the mail, which has saved us on postage and time spent.

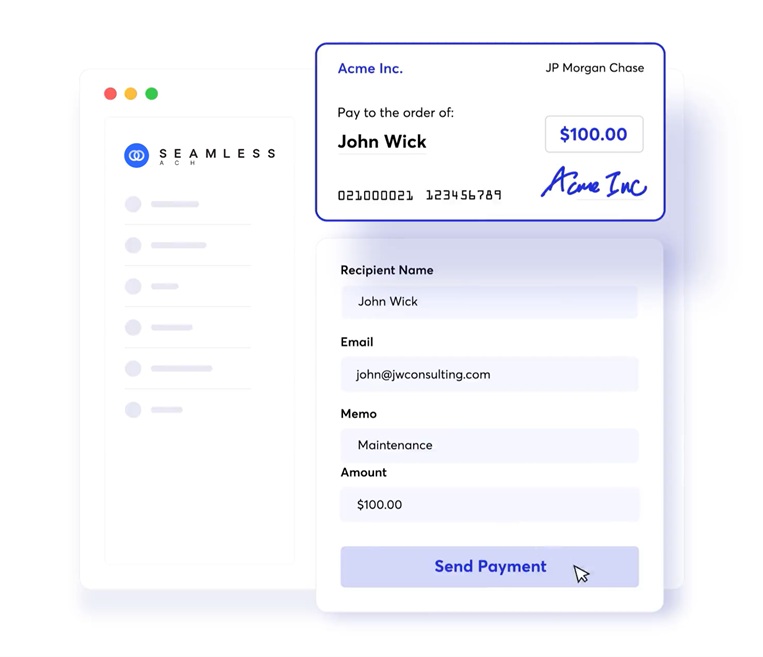

An all-in-one bank payments platform that lets merchants add Pay by Bank to checkout, accept verified ACH debits, and send instant payouts—while built-in verification helps reduce fraud, returns, and payment risk.

Sign Up Now

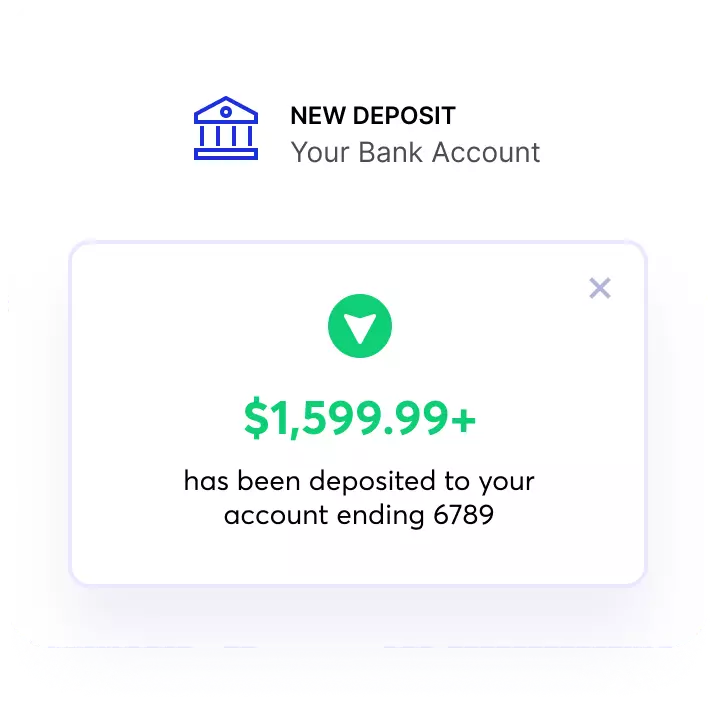

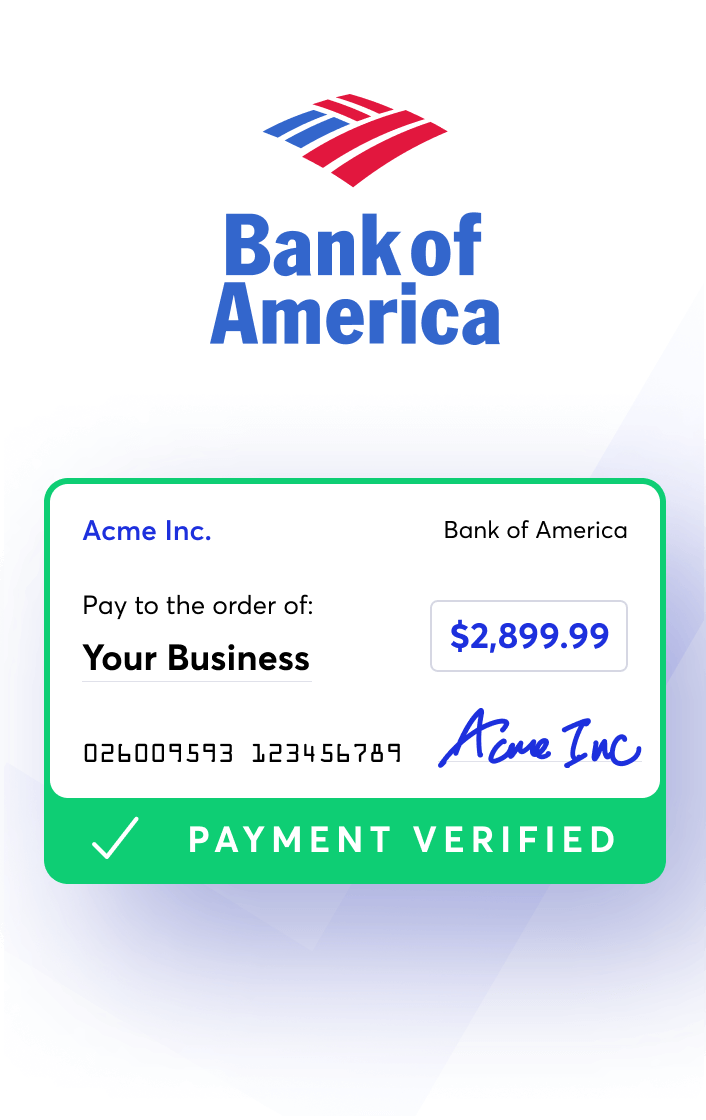

Seamless ACH enables instant account setup with real-time bank verification to confirm account ownership and reduce risk. Once live, merchants can process same-day ACH debits or send instant RTP payouts—all from a single platform.

Start sending and accepting Bank payments today

Faster pay-ins and instant payouts for modern gaming experiences.

Seamless ACH lets gaming platforms add Pay by Bank at checkout for lower-cost deposits, then send instant payouts to players via real-time transfers. Built-in bank verification and risk controls help reduce fraud, chargebacks, and failed transactions—so players can deposit and cash out quickly without creating new accounts or using third-party wallets.

Lower-cost checkout with faster access to funds.

Seamless ACH enables ecommerce merchants to accept Pay by Bank payments at checkout, reducing card fees while improving approval rates for high-value purchases. With verified ACH debits, same-day settlement, and instant payouts for refunds or incentives, Seamless ACH helps ecommerce businesses move money faster while minimizing risk and returns.

Recipients will never need an account or app to pay your invoice or receive a payment.

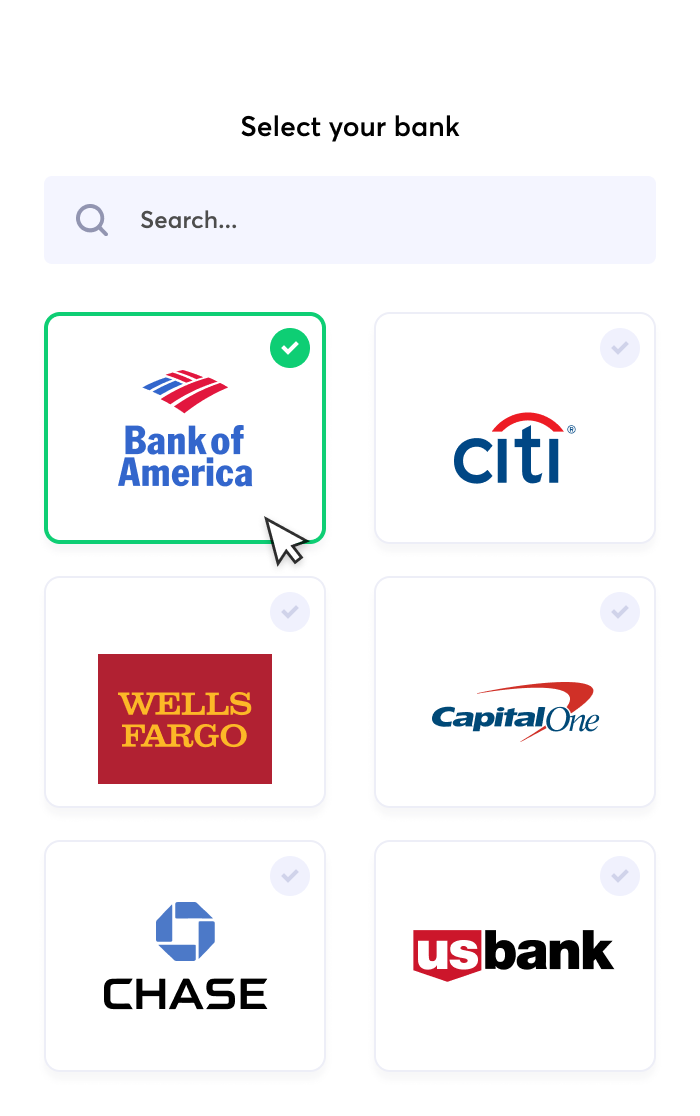

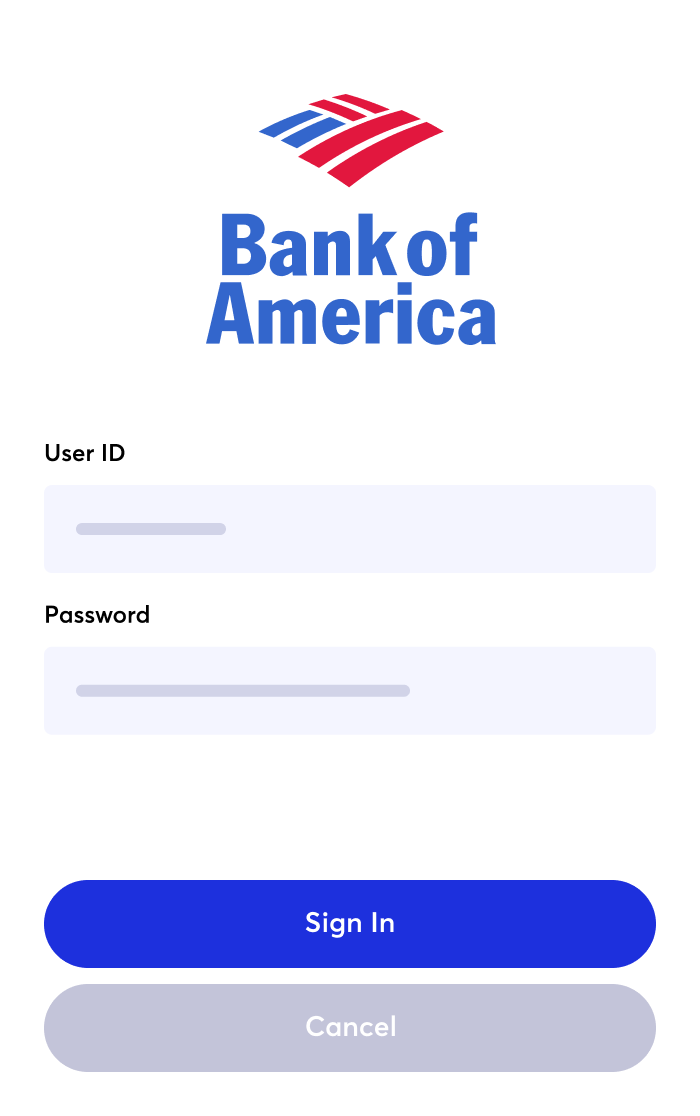

Seamless ACH securely connects to your bank. No need to share sensitive account information.

Clients just click on the link in the email, connect to their bank account, and pay the invoice.

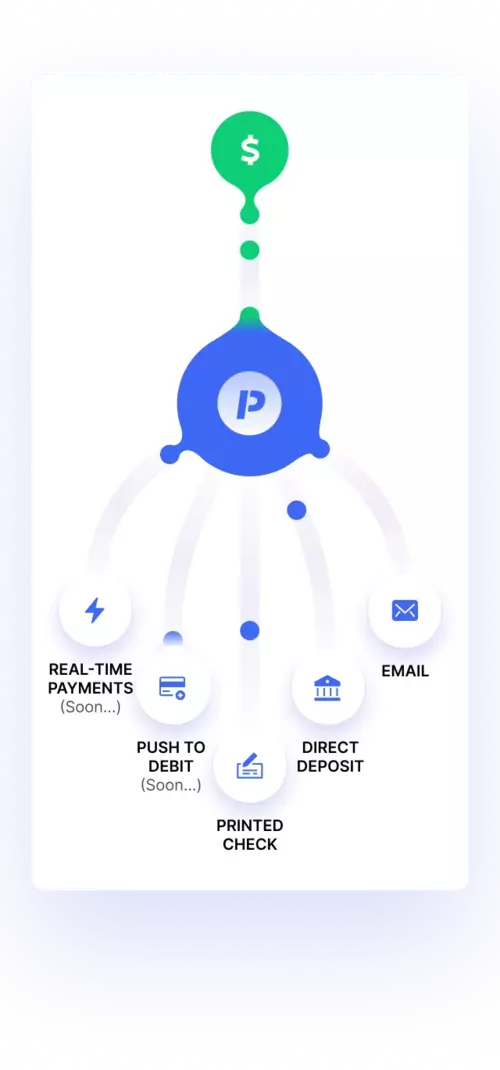

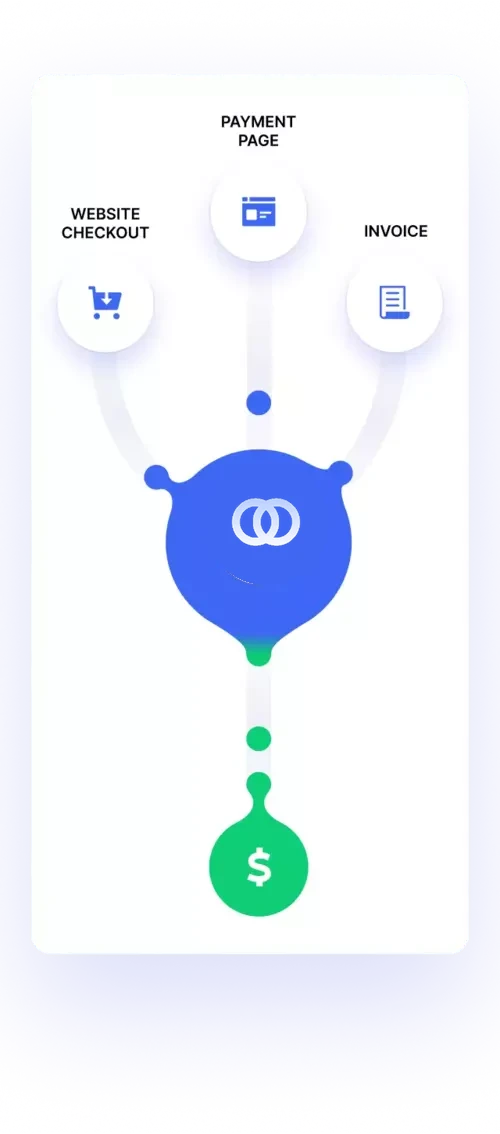

Send money online instantly, no matter the method. Just about anything you can pay by check, credit card, or bank transfer can be paid online with Seamless ACH:

As a business owner, Seamless ACH has helped to significantly reduce the number of checks we have to put in the mail, which has saved us on postage and time spent.

Seamless Merchant has been a great asset to our organization for the past 5 years. They are always quick to respond and a pleasure to work with.

Seamless Merchant has been great at keeping our payment processing fees at an absolute minimum.

Thanks to the insightful advice and great service offered by the team at Seamless Merchant, our ecommerce business operates more efficiently.

eCheck verification has reduced returned checks for our clients by 63% resulting in thousands saved on bank fees. They also offer A+ developer support!

Very reliable verification and great customer service. Customer Support is always responsive and available.

We have over 90 locations and Seamless Chex helps us collect out money faster, easier and more efficiently.

Excellent service! Sending invoices with Seamless ACH has significantly reduced A/R by letting our customers pay online.

SeamlessChex helped us solve one of the crucial problems we were having as a business: recurring payment to vendors.

Seamless ACH allows us to easily request one time and recurring rent payments from our tenants.

SeamlessChex has made it easy for our business to receive funds the next day from our clients.

Every small business needs Seamless ACH! Seamless ACH's allowed me to send and receive payments quickly, securely, and reliably.

SeamlessChex has been an invaluable addition to our company. It has drastically reduced the time to receive.

To accept ACH (Automated Clearing House) payments online, follow these four steps:

1. Set up a Merchant Account

The first step is to set up a merchant account with a bank or payment processor, like Seamless ACH, that supports ACH transactions

2. Gather Customer Information

Collect the customer information you need to process ACH payments. This usually includes the customer's name, bank account and routing number, and address. You'll also need authorization to debit the customer's account.

3. Choose an ACH Processing Method

Next, choose the ACH processing method that suits your needs. Here are a few of the most common:

4. Implement ACH Payment Processing

Finally, follow the provided instructions on your chosen ACH payment method. These instructions will allow you to integrate the ACH solution into your website or system and start accepting ACH payments online.

If you want to accept ACH payments, you need a merchant account or an account with a payment processor that supports ACH transactions.

These accounts are provided and supported by banks or third-party processors, like Seamless ACH, which may enforce their own eligibility requirements and restrictions - depending on the provider you choose.

While individuals and businesses can usually set up ACH payment acceptance systems, it's important to note that the significant requirements vary.

Some payment processors, for example, require a particular duration of business history or a specific level of creditworthiness or transaction volume before they allow you to start accepting ACH payments.

To set up ACH payments on your website, follow these seven steps:

In addition to the steps above, remember to review and comply with all legal and regulatory requirements associated with receiving ACH payments in your jurisdiction.

While the steps above are a general guideline, it's important to note that specific steps may vary depending on the website platform you're using and the ACH payment processor you've chosen to integrate.

As such, we recommend consulting your payment processor's documentation and support resources since these documents will provide more detailed integration instructions tailored to their services.

There's no one-size-fits-all rule for how much ACH payments cost. In fact, the cost changes depending on variables like which payment processor you're using, which merchant service provider you choose, and your specific business needs.

Here are some common variables to consider:

Whenever you're evaluating ACH payment software, it's critical to research and compare pricing structures and fee schedules to find the payment processor that best suits your business needs. Consider factors such as transaction volume, average transaction size, and other specific requirements you or your business may have.

The terms ACH Payment (Automated Clearing House Payment) and EFT Payment (Electronic Funds Transfer Payment) are often used interchangeably. What most people don't know is that they are not the same thing.

Here's a quick breakdown of the differences between the two:

To sum it all up, the term ACH payments refers to a specific type of EFT payment that utilizes the ACH network in the United States. The term EFT payments, on the other hand, refers to a much wider range of electronic funds transfers, including but not limited to ACH. EFTs can be conducted domestically and internationally through various electronic payment networks and systems.